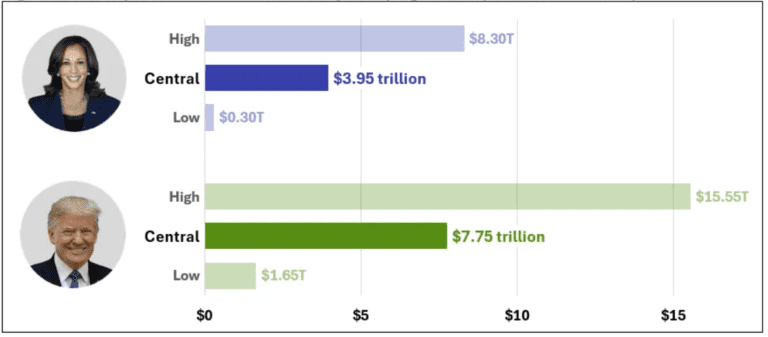

One area where the candidates do diverge is in their approaches to raising revenue. Harris, generally in alignment with Biden’s policies, favors higher taxes on high-income earners and corporations. In contrast, Trump advocates for broad tax cuts and aims to compensate with increased tariffs—a relatively novel approach for the U.S., which hasn’t relied significantly on tariffs for revenue in recent years.

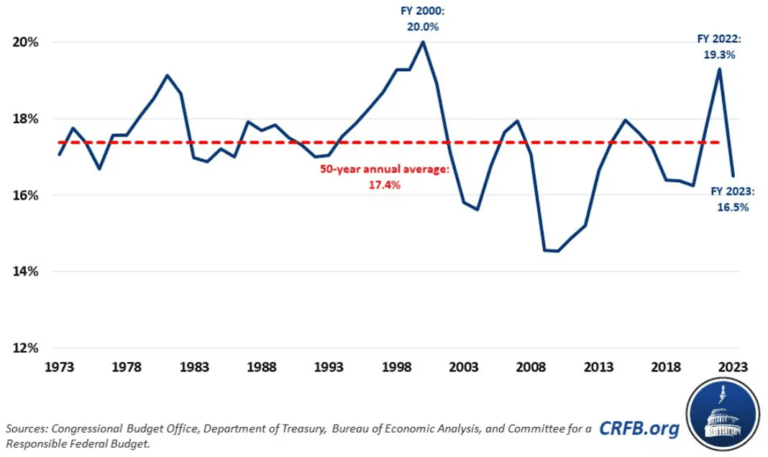

Despite their differences, the actual revenue impact of both approaches has remained close to historical averages over the last eight years. The one notable exception came when revenue surged between 2021-2022, driven by capital gains taxes as a result of the Covid-related economic stimulus, low interest rates, and speculative market activity. However, this increase was a temporary spike arguably not related to tax policy, and revenue has since returned to traditional levels.